Schumacher Center for a New Economics, 140 Jug End Road, Great Barrington, MA 01230 Email: schumacher@centerforneweconomics.org Phone: (413) 528-1737

School of Living, 215 Julian Woods Lane, Julian, PA 16844 Email: schoolofliving@gmail.com Phone: (814) 353-0130

The Papers of Ralph Borsodi

Articles, research files, and previously unpublished manuscripts of Ralph Borsodi can be viewed at the Schumacher Center for a New Economics Library. The materials in this special collection were acquired from the files of Borsodi’s former editor Lydia Ratcliff. Ralph Borsodi (1886-1977) was an economist as well as an author and founder of the School of Living in 1934. In the early 1970’s, Schumacher Center founder Robert Swann worked with Ralph Borsodi to issue Constants, a commodity-backed currency, on an experimental basis in Exeter, New Hampshire. The Exeter experiment began in April 1973 and ran for over a year, circulating almost 100,000 Constants in Exeter, Borsodi’s hometown. Borsodi and Swann were two of the most influential intellectual leaders of the community land trust movement in the United States. Together, they established the International Independence Institute in 1967 to provide training and technical assistance for people who were interested in promoting rural development.

The Milne Special Collections and Archives at the University of New Hampshire Library in Durham, NH houses Ralph Borsodi’s papers from 1938-1977. This collection consists of correspondence, much of which concerns the imminent visit to the United States of Jayaprakash Narayan in 1966; manuscripts for several of Borsodi’s works, both published and unpublished; and a small amount of papers from the School of Living, the University of Melbourne, and the corporations that Borsodi set up to implement his ideas.

Table of Contents

Introduction by Robert Swann Chapter 1: The Blind Leaders of Our Blinded World Chapter 2: Keynesianism Chapter 3: The Story of the Escondido Memorandum Chapter 4: The Exeter Experiments Chapter 5: On the Nature of Inflation Chapter 6: On the Nature of Money Chapter 7: On the Issuance of Money Chapter 8: On the Redemption of Money Chapter 9: On the Nature of Measures of Value Chapter 10: On the Nature of Bank-Money Chapter 11: On the Nature of Paper-Money Chapter 12: On the Nature of Metal Money Chapter 13: On the Nature of Arbitrage and of Speculation Chapter 14: On Currency Arbitrage Chapter 15: On Commodity Acquisition, Arbitrage, and Lending Chapter 16: On the Nature of Lending and Investing, and of Speculating and Exploiting Chapter 17: On the Acid Test: Deflation Chapter 18: On the Nature of Banking Appendix A: Statistical Problems Appendix B: On the Wording of Paper-Money Appendix C: The Escondido Memorandum Appendix D: Bibliography

Introduction by Robert Swann

Ralph Borsodi once said that without money reform, no social reform would be possible, and he added money reform, or an honest money system, will be the most difficult reform to bring about because so few people understand the problem. Because Borsodi was and is a widely recognized leader of the decentralist movement in the United States, and because his books, from The Distribution Age to Seventeen Problems of Man and Society represent such a comprehensive analysis of our present society, such a statement has to be taken seriously.

At the same time he was reluctant to write a book about it. It was only after he had almost single-handedly launched the “Exeter Experiment,” as he called it, that some of us who were working with him persuaded him to set down in a brief outline his ideas for an “honest money system” which are contained in the pages which follow. He had, in fact, in 1977 at the age of 87, set out to write a book on what a “decent” money system would look like. At the same time he was on a trip in California and he had gone to the library to do some research for the book. But when he noted the headline in a local paper which announced that inflation had increased another percentage point in the last month, he decided that another book would be useless. There were too many books already. No one would pay any attention to another book. He sat down and jotted what he later called the “Escondido Memorandum.” It was an outline for action on how to establish an experiment which would actually launch an “honest money system.”

On returning to his home in Exeter, New Hampshire, he sought out the president of the local bank, a good friend of his, and asked for his cooperation. His plan was to announce in the local newspaper (the publisher was also a friend) that he, Ralph Borsodi, would indeed issue a currency based on 30 commodities, and this currency could be purchased with U.S. dollars at the local bank, and would be accepted as payment for goods at local stores. He noted that the currency would not devalue like U.S. dollars because it could always be redeemed for the same amount of commodities, or it could be redeemed at the local bank for U.S. dollars at an exchange rate based on the current price for the index of commodities. Since the “commodity basket” as he called the currency, would continue to have the same value, even as the dollar went down in value. Hence, it would take an increasing number of dollars to exchange for the same number of constants. To ensure there would be enough dollars in the bank, he placed some of his own money with his friend at the bank to cover any demand.

During this period he talked with local store owners to get their support and set up regular meetings for local people, especially business people, to explain how his system worked or the concept in back of it. All of this work and education paid off, and to his own surprise many people began buying “constants” and using them at local stores. Even the Town of Exeter accepted them as payment for parking traffic fines. Very few people ever redeemed them for dollars at the bank.

In order to continue such a scheme, of course, it would have been necessary to purchase significant quantities of the 30 commodities which were included in the basket. An initial start was made by purchasing a quantity of silver, but this was later sold to cover the cost of returning dollars for Constants, when Borsodi had to give up the experiment partly due to his age and health. Many people never did turn in their Constants, probably keeping them as souvenirs of the “Experiment.”

What was the result of the experiment? Borsodi had proved what he had set out to accomplish: that people were interested in a currency which did not devalue. The media was quick to realize how interested people were. Two national magazines, Forbes and Newsweek, carried stories about it and several newspapers in the region wrote about it.

But what would be necessary to bring about a wide scale monetary reform? What would an entire money and banking system which would change, in fact revitalize, an entire economic and social system, look like? These were the questions we asked Borsodi, and we finally got him to sit down and draft in his terse, curmudgeon style the following essays on money and banking.

Chapter 1: The Blind Leaders of Our Blinded World

Very appropriately on April Fool’s Day, on April 1, 1974, the New York Times published on its first page one of the most extraordinary stories which has ever appeared in a modem newspaper. Since the New York Times is the most widely read newspaper in America and perhaps the most influential published in the whole world, this must be an extraordinary story to justify making such an extraordinary statement about it.

The story was written by Soma Golden of the Financial Department of the Times. It is devoted to the fact “Inflation Grips the United States”, as one of its headlines states, and the fact that the leading economists of the nation do not know what to do about it. As Paul C. McCracken, who was Chairman of the Council of Economic Advisers early in the Nixon Administration puts it, “high probability” must be given to the notion that “modern societies do not have the knowledge and the will to keep the price level reasonably stable”—that neither the economists, who provide societies with their knowledge about money, nor the bureaucrats and bankers, who put that knowledge to work, know what to do or are willing to do anything which will “curb inflation.”

Golden quotes the nation’s leading economists and monetary authorities—including Secretary of the Treasury George P. Schultz; Walter W. Heller, who was Chairman of the President’s Council of Economic Advisers in the Kennedy and Johnson administrations; Henry Kaufman, a leading Wall Street economist; Milton L. Friedman, of the University of Chicago; James Tobin, of Yale University, a member of Kennedy’s Council of Economic Advisers; and Arthur Okun, another former Chairman of the Council of Economic Advisers. He sums up what they have to say as follows:

After years of slowly rising prices and seeming immunity from the virulent inflation elsewhere, the giant and troubled American economy stands poised in the middle of an inflationary spiral.

Economists are stunned by it.

They do not agree entirely on what to do about it, according to Golden. Many of them admitted that they did not know what to do about it at all.

Even Milton Friedman, who is one of the few distinguished economists in the United States who is not a Keynesian and who expects that United States inflation will begin soaring steadily at a rate of 10 to 12 percent, came up only with an expedient which accepts inflation; none of them proposed anything to stop it, and none offered anything except the hope that it might be reduced.

Let’s face the facts: the men who are actually leading us, who are responsible for what is going on, who are making the decisions about what is to happen, are confessing their blindness. The economies of the West, headed by that of our own, are heading for catastrophe led by blind leaders of a blinded world.

***

We are being victimized by so-called authorities who are what Pitirim Sorokin called “amnesiacs.” They are men so absorbed in what is happening and what is being said today—whose noses are so close to the grindstone—that they have lost all knowledge of what was written and what happened in the past. They are men who have never heard, apparently, of Samuel Jevons or Irving Fisher, or of F. A. Hayek or Frank D. Graham, of Jan Goudrian or Benjamin Graham, of Henry George, of Horace White, of Louis D. Brandeis, of Thomas Jefferson and Alexander Hamilton.

They are men who have apparently never heard or never read, or forgotten what they have read, about the ideas of these men. They are men who know all about the minutest details of what is considered economics today but not that in economics as in everything else, ends dictate means, and that if ends are wrong, the better the means used to realize them, the worse the result.

They have forgotten their histories. They do not know that in the conflict of ideas about the American dream, it was Jefferson who lost and Hamilton who won. They do not know that Jefferson’s goal was democratic, Hamilton’s plutocratic. They do not know that Jefferson believed that the freedom, the justice, and the integrity he wanted could only be realized in an agrarian and decentralized society. They do not know that Hamilton believed that the rich and powerful America he wanted, called for the creation of an industrialized and urbanized nation. Above all they do not know that Hamilton succeeded and Jefferson lost because Hamilton laid the foundation for the monetary and banking confusion which bedevils us to this day. Finally they do not know that in the conflict between the original American dream of a free economy, a free polity, and a free society on one hand, and the Socialist and Communist dream of planned and regimented prosperity on the other, it is the Socialist dream which is certain to prevail unless by some miracle the moral equation is injected into the resolution of the crisis we face today.

They write their text books, they teach their classes, and they advise the government about what it should do as if all the basic problems of how to avoid inflation had not been solved long ago when Jevons and Fisher called attention to the significance of index numbers, and as if some of the best economists of all time had not advocated the issuance of commodity-backed currencies so as to provide a constant value for the unstable and variable so-called “standards” of value of the past.

They certainly never heard, or if they have, have forgotten what Henry George made clear in Progress and Poverty, that unemployment is a pseudo-problem; that it has troubled and is troubling mankind for only one reason, because self-employment and in effect full-employment is made impossible by the expropriation of land and the prevention of access to it without prior payment of tribute to the land-speculators who own it.

All of the economists and authorities Golden quotes in his story are “amnesiacs.” What all the Keynesian economists are teaching us, out of the Keynesian economic textbooks which they use, consists of pseudo-economics. None of them are willing even to consider repudiating those who have and are misleading and bamboozling the world, and of turning to an alternative which would make it possible to escape from the catastrophe toward which they are leading us.

There are four things which all these economists and all the officials and bankers who are responsible for our monetary policies ignore:

The first is that inflation is dishonest. It is a form of embezzlement. What is worse, it is a form of legalized embezzlement. Those who ignore this fact in effect condone it. And there is no excuse whatever for condoning any form of stealing.

The second fact is that the inflation is deliberate. It was planned. It is in actuality a sort of conspiracy entered into by nations and those who represented and participated in the International Monetary Conference held in Bretton Woods, New Hampshire in 1944. It is an ongoing conspiracy still being carried out by all the nations which are members of the International Monetary Fund. The dishonesty involved is therefore deliberate.

The third is that it is unnecessary. None of the so-called reasons, none of the excuses and rationalizations of those who are responsible for the inflation or who condone and justify it, have any real validity.

The fourth and final fact is that almost without exception those leaders of the world who say that they are against inflation and who claim to be fighting against it, are lying. It is a lie to say that you are against something which you are in truth advocating. It is a lie to say that you are against something which you are in fact deliberately doing. It is a lie to advocate doing a little of what in fact should not be done at all. It is a lie to say you are against stealing, when you are in fact saying that a little stealing is all right. It is a lie to say that a little inflation, say two or three per cent, is not stealing but that a lot of inflation, say ten or twenty or thirty percent, is all wrong.

They do not therefore know that Keynes was wrong when he persuaded the whole West to accept his doctrine that the only way to ensure economic growth and to abolish unemployment was to use inflation. They certainly do not know that it is wrong from every standpoint except that of immediate political expediency. It never therefore occurs to them that the real problem is not how to “curb” inflation— how to reduce it or how to prevent it from running away— but how to stop it altogether. Even less does it occur to them that inflation will be neither curbed nor stopped until some alternative is offered to the existing inflation-prone currencies of the nations in the IMF, and that it is made possible for people to turn to a currency which is inflation proof—a currency based upon some such solution of the problem which in the Exeter experiment I called a constant. When that becomes possible we will have Gresham’s law operating in the reverse—good money will be driving bad money out of circulation.

Chapter 2: Keynesianism

The architect of the inflation with which the world is faced was John Maynard Keynes. Those initially and currently responsible for it are the organizers of the International Monetary Fund and their successors.

Ultimate responsibility, however, belongs to the leaders and teachers of the free world who, if they did not, should have known the truth about it, and if they did, utterly failed to make it known. A short excursion into history will make this clear.

The Coinage Act of April 2, 1793 made the dollar the legal unit of currency and legal tender in payment for all debts in the United States.

The Act provided that dollars issued by the United States should be redeemable by the Treasury Department in 24.75 troy grains of fine gold or 371.25 of fine silver.

As the accompanying chart makes clear, the dollar’s purchasing power at that time was equal to 100% of what this quantity of gold or silver would buy. It fluctuated between 75% and 85% of its original purchasing power until the War of 1812. During that disastrous war it dropped as low as 56%. It not only recovered but during the 1820’s it rose way above its original purchasing power.

The history of its purchasing power for the first one hundred fifty years of its existence can be described as one of ups-and-downs fluctuating around its original purchasing power. But then in the 1940’s something happened which completely changed its history.

What happened?

Two things happened: (1) The International Monetary Fund was organized in July 1944 at the famous Bretton Woods Conference, and (2) Keynesianism became the dominant monetary policy of all of the nations which became members of the IMF. There was no explicit endorsement of Keynesianism by the Conference or by the IMF, but for all practical purposes the conference set the machinery to Keynesianize the West in motion.

Since then, the chart not only records what has happened to the dollar, it points to what is going to happen to the dollar since nothing has been done to change the direction in which the dollar is going. In the first place, in the more than thirty years since this double “happening” the dollar has fluctuated but always fluctuated downward in purchasing power. Today, as I write, it has less than a third of its original purchasing power. In the second place, as I have already pointed out, there is nothing in sight but more and more inflation and less and less purchasing power.

Neither of these two happenings contributed a particle to making the dollar a more stable currency unit. Had the Coinage Act of 1793 provided for a stable currency, or had any subsequent act dealing with the currency provided such a currency, the purchasing power of the dollar would have begun to fluctuate in all probability not more than one or two percent around a level—neither a rising nor falling—secular trend. It would have been neither inflated nor deflated and it would not have developed the downward secular trend which began early in the 1940’s. The chart makes vividly clear the long-time trend of increased inflation and de creased purchasing power of the dollar. It makes it clear that since this double “happening” the money managers of the country have, for all practical purposes, been engaged in murdering the dollar.

***

When the history of the mis-education of mankind is finally written, few of the outstanding mis-educators will outshine John Maynard Keynes. Ironically, Keynes was knighted for both his disservice as a mis-educator and his disservice as an economic activist.

It is a tragedy that the rationalizers of economic half-truths and economic expedients (which are rarely truly expedient) should be accepted not only by the general public but also by professional economists who should have spotted their phoniness immediately. Competent economists should all have denounced Keynesianism as charlatanism— a charlatanism made worse by the moral naiveté of Keynes and his devotees who were and are still unconscious of its nature. The Keynesians, however, are sophists who have no difficulty in the present climate of economic opinion in “making the worse appear the better written.” The eminence of so many of them and the influence they exercise both in Washington and in Wall Street only proves the credulity of those who should have highly developed talents for skepticism.

Will the price we will have to pay to disillusion the West about Keynesianism be as great as the price paid by those whose faith in the New Era of the 1920’s was destroyed during the worldwide economic collapse of 1929?

Will the price we will have to pay be greater; will it be not only the collapse of the dollar and with it the collapse of the whole IMF, but also some form of fascism, or —

Will it mean that the price we will have to pay will also include some such revolutionary hell as Lenin and his cohorts visited upon Russia and which the other “dictatorships of the proletariat” are now inflicting upon the rest of the totalitarian Communist world?

What the International Encyclopedia of the Social Sciences says about the Keynesian revolution is very true: “It is generally agreed that the impact of John Maynard Keynes on the development of economic theory was greater than that of any other economist in the first half of the twentieth century”.

Yet everything he wrote and everything that he succeeded in doing has to be considered in the light of the fact that he was so obsessed by his fears about the problem of unemployment that he did not hesitate to rationalize and encourage unleashing the scourge of planned inflation.

For Keynes, providing prosperity and full employment justified deficit spending and payment for it with inflation. The tactics he recommended can be likened to that of a doctor who is confronted with a man shivering in bitter wintry weather and infects him with typhoid so as to make certain that he has a high fever. The fever will certainly make him feel warm, but consider the price his patient will have to pay for that short period of warmth!

Keynes was too intelligent a man not to realize that he was monkeying with fire. He himself once said:

Lenin…declared that the best way to destroy the Capitalist system was to debauch the currency…Lenin was certainly right. There is no subtler, no surer way of overturning the existing basis of society.

Yet I can think of no man who, with the best intentions in the world, has done more to “debauch the currency.”

Like most economists, Keynes labored under the delusive notion that ethics and economics have nothing to do with one another. He was perfectly willing, therefore, to prescribe legalized robbery by the government of every person who had a savings account, who held a life insurance policy, who had savings invested in bonds, or who lived on a pension. Debasing the value of money and reducing the purchasing power of people’s salaries and savings is a very subtle way in which the government quite legally either appropriates what the people lose or transfers it into the pockets of those the government wishes to favor. True, Keynes wanted this done with restraint, and only when needed to stimulate employment, but he ought to have known that no government in any way beholden to the masses of people would exercise such self-control.

Keynes, like most economists, had not the remotest notion of what was the correct solution of the problem of unemployment. He took it for granted that anyone who was unemployed had the right to demand of the government, “You furnish me a job!” If he ever read Henry George, the fact made no impression upon his thinking. He did not realize that involuntary unemployment was impossible in a society in which the system of land tenure gave everybody equal access to land. Even Marx admitted that there could be-no surplus of labor until land had been first preempted by private owners.

Men are not born with any natural right to employment by others. The only natural right they are born with is the right to extract a living from the cultivation of the earth. Resorting to an expedient like inflation to provide employment is no substitute for justice—and justice is denied to everybody under a system of land-tenure which makes it possible for a few to preempt land and resources which should be accessible to everybody who is willing to pay ground rental for it.

Keynes cannot be said to have belonged to a school of economic charlatanism such as that represented by W. H. (Coin) Harvey, whose book, “Coin’s Financial School” was sold by the hundreds of thousands during the panic of 1893. Nor to a school such as that represented by “General” Jacob S. Coxey who organized a march on Washington to demand the printing of an unlimited quantity of greenbacks so as to put the country “back on the tracks” to prosperity. The constantly increasing numbers of marchers in Coxey’s army when they finally reached Washington scared the living daylights out of Congress and the Administration.

It is more correct to say the Keynes created a school of economics such as that created by Major C. H. Douglas with his scheme for Social Credit. But he was much more clever and therefore more dangerous.

***

This is not a history. No historical account of the Bretton Woods Conference is needed for this study. But there are a number of things for which the Conference was responsible and a number of facts about the Conference which are germane.

The first is that it was important. It dealt with a problem of first-rate importance. Secondly, it set up an organization, the International Monetary Fund (IMF), which used the dollar as a reserve currency. With splendid unrealism it assumed that the United States would always redeem its dollars in gold at $35 an ounce. Thirdly, it made an agreement, presumably to be a permanent agreement, about the rate at which the various currencies belonging to the Fund would be exchanged. No matter how many times since then this agreement has broken down because of the revaluation of the pound, or the franc, or the mark, or the yen, it kept on making the same kind of “permanent” agreements. After all these years, it has still not learned that agreements for fixed exchange rates will not last. Fourthly, it implicitly, if not explicitly, accepted Keynesianism—the issue of money by its members to ensure full development and full employment.

Since that time, as Jacques Rueff points out with biting irony, it has learned nothing from its previous failures and so repeated them at the Smithsonian institute Conference in Washington when the dollar was devalued.

The IMF has really only done one thing new—it created “paper” gold to use as a reserve when it discovered that the United States simply could not redeem its promise to redeem dollars in gold. That economists today, in the twentieth century, could take the concept of paper gold seriously shows that they have forgotten all about what they used to say about fiat money during the nineteenth century.

On the whole the record proves that the members of the IMF are all champions of expediency and not champions of what is economically sound and morally right.

That there are economists who try to escape from pseudo-economics is demonstrated by Irving Fisher.1 His interest in macro-economics dominated his life; his interest in microeconomics was minimal. An activist as well as a theorist, he organized the Life Extension Institute, which became a great success, and the Stable Money League, which did not. He tried to persuade the whole fraternity of the importance of stable money. I had the pleasure of trying to help him a little during the Great Depression in the 1930’s when he was trying to create a workable scrip when money was almost unobtainable. But it was his work on index numbers which I consider outstanding. I believe him to be as greatly underestimated as Keynes has been overestimated.

Ever since Stanley Jevons in England published a paper which he called “A Serious Fall in the Value of Gold” and began to use index numbers to measure changes in prices, there has been no excuse for the failure of economists to use them as a means of establishing a stable unit for monetary measurement. Since Fisher’s exhaustive work in this field, there is not a single technical problem which cannot be solved in connection with establishing a stable dollar, a stable pound, a stable mark, or a stable franc. The problem which is insoluble is how to get politicians to give up the political leverage inflation provides for keeping them in office, and how to get investment bankers to give up the leverage it provides for launching securities when prices are going up. In a way this is only saying that not only does the quest of power corrupt but that the quest of greed is equally corrupting.

So far as economists are concerned, they already know how to establish a stable currency unit—for statistical purposes. Don’t they already distinguish between what they say in constant dollars from what they say in current, variable and inflatable dollars? Index numbers make it possible to do this, but they make it possible to do much more—they make it possible to issue a stable money. If constant dollars are ever to be moved from the charts and statistics and from the books and papers which abound in the abstract world in which economists live into the real world in which people earn and spend and buy and sell, economists must give up expedients and palliatives like Keynesianism and accept the fact that nothing short of replacing our rubber monetary units with stable monetary units which have a constant purchasing power, will do.

***

Among the cynics of today there is a saying: “statistics do not lie, but statisticians do”. In the preparation of the chart describing the history of the dollar, I discovered that what used to merely irritate me was in fact a means of misrepresentation, of concealing the truth, of—to use a short and ugly word—lying. I have always been irritated by the frequency and the variety of the “base years” used in statistical tables and charts. When I wanted to prepare a single graphic chart to show what had happened to the dollar since it came officially into existence, I was faced with four sets of base numbers. The only available data consisted of four sets of Wholesale Price Indexes with four different base years: 1910-1914=100; 1926=100; 1947-1949=100, and 1957-1959=100. To convert them into a single table was a tedious, tricky and irritating job.

The current issue of the “Survey of Current Business” uses still another base year to show the movement of prices, 1967=100. Why all these changes? To mystify? Why do statisticians and economists change these base years for the indexes which purport to show the cost of living and the purchasing power of the dollar? Why do they change them more and more frequently since inflation has become a part of the American Way of Life?

The fact is, their changes make it easier to misrepresent the facts, to avoid the truth, to lie in the meanest way—by telling a half-truth. The truth about the matter is that if the increase in wholesale prices which was shown as 115 on a 1967 basis had been shown on a 1926 base, the figure which would have had to be used would have had to be around three times as much, 445—a figure so startling as to focus attention upon the real magnitude of the inflation with which the Country is cursed.

The base year I am using in my chart is 1793—the year the dollar came legally into existence. The chart makes a graphic presentation of the fact that since Keynesianism took over, Washington has been murdering the dollar. No wonder there is an undercurrent of unease even in Washington. Unconsciously Washington knows that we are sitting on a time-bomb and that the moment something happens so that confidence in the dollar is threatened, something like 1929 will repeat itself. They talked about a “New Era” before the Great Depression. They are not calling the present period a New Era today. But the psychological climate is the same— everybody has been conditioned to feel that the laws now regulating money and banking make a repetition of anything like 1929 impossible.

I wonder. The nature of technology changes; we now use atomic bombs instead of bows-and-arrows. But the nature of the human animal does not—or changes so slowly that for all practical purposes it does not change at all.

There is another “lie” to which I think it worth calling attention—an inadvertent rather than a deliberate lie. This is the lie represented by the use of the word inflation. The word suggests something getting bigger—when a balloon is inflated, it becomes bigger. But they are not inflating the dollar in Washington, they are degrading and debasing it. They are increasing the quantity, but they are debasing its quality.

It would be a very healthy thing if we substituted the word debasement for the word inflation whenever we talk about what Washington is doing to the dollar. If the politicians in both parties were to start accusing each other of responsibility for debasing the dollar, politicking would be much more realistic.

I have referred to what is being done in Washington as murdering the dollar. But murdering of the same kind is taking place all around the world—from Washington to Tokyo, on the other side of the world. In 1971, prices in the United States went up 6.2% but in Sweden they went up 6.3%, in Japan 8.3%, in Brazil 21,7%, and in Chile 29.3%. Said a Swiss economist:

The greatest trouble for the world now is American inflation. If the United States, with its powerful economy and the world’s leading currency cannot hold its rate of inflation below 5 to 6 percent annually, what hope is there for the rest of the world to restore stable conditions?

For nearly 200 years the farmers, the businessmen, the manufacturers, and the rank and file in America have labored under an incubus which alternately inflicted upon them the miseries of “hard times” and then spasms of wild speculative prosperity. The record constitutes a blistering indictment of bankers, politicians, businessmen, economists, statisticians and everybody who has had anything to do with the issuance of money. It is no exaggeration to say that the free economy, which the founders of the Republic considered essential to the building of a free society, is foundering.

The vision of a world composed of free nations may finally fade out because of the mishandling of their monetary systems. Among the principal culprits responsible for this will be those in power in the Wall Streets and the Washing-tons of each free nation—the bankers and the politicians who have issued and managed their currencies. It is they who should be held responsible for the sorry record to date and they who should be pilloried for what they are continuing to do at present.

The United States Treasury Department produces detriments and not goods by issuing money and inflating the quantity of it with the assistance of the Federal Reserve Board and all its member banks throughout the country.

It alternately expands and contracts the supply not in accordance with the needs of the economy but in accordance with the needs of Washington at best, and in accordance with the needs of Wall Street at worst. So intimate is the tie between Washington and Wall Street that it is difficult to decide to whom to assign the major responsibility for the debasement and murdering of the dollar. But that these two centers do bear the major responsibility is incontestable: Wall Street by printing insecurities and the Treasury Department in Washington by printing dollars. Wall Street issues pseudo-securities and Washington pseudo-money. Similar centers exist in all the large industrial nations of the world. England, with the appearance of the Industrial Revolution, pioneered in pseudo-production. Japan is the latest present-day industrial nation to join in the game of pseudo-production. No doubt others will arise until the last of the free economies disappear, and the verdict of the Inquest of History upon what Lincoln called “the last great hope of mankind” will be death by monetary suicide.

I will throughout this study stress the fact that neither Wall Street nor Washington should have any part in or control over the issuance of money. To make clear what I mean when I speak of Wall Street and Washington, it is necessary to distinguish between what they in theory are supposed to be and what they in fact are.

Wall Street, in theory, is the center of the financial system which provides properly and effectively for the capital needs of the nation. But Wall Street is in fact a speculation center organized and operated for the purpose of enabling a self-selected minority of men and of boundless greed to become millionaires and billionaires. Whatever Wall Street does to provide for the capital needs of the nation is incidental to, and misshaped and distorted by, what it in fact is.

Washington, in theory, is the establishment which governs the nation for the purpose of providing for the protection and for the welfare of the people it governs. Washington in fact is an establishment misshaped and distorted for the purpose enabling men of boundless ambition to gratify their desire to exercise power and to exploit it as long as they can.

In theory the functions which the two perform are entirely different. In practice, however, both the men of greed and the men of power have found that they can gratify their desires far more effectively if they work together. In practice, Wall Street and Washington operate as if they were Siamese twins. And this is the way they are both operating in dealing with Keynesianism.

Chapter 3: The Story of the Escondido Memorandum

On September 15, 1943, in the middle of World War II, I spoke about inflation at a dinner meeting attended by over five hundred people at the historic Aldine Club in New York City. The Chairman who presided was Dr. William H. Kirkpatrick, Emeritus Professor of Education of Columbia University; I was introduced by Pearl Buck, then one of the leading novelists of the day and a distinguished Sinologist. After my talk, a panel of equally distinguished authorities in many different fields discussed my prediction that after the war inflation would cause a depression of catastrophic consequences.

Five years later I wrote for the publishing division of the School of Living what today would be called a paperback. It embodied most of what I said at the Aldine Club in 1943. It was entitled “Inflation is Coming! and What To Do About It”. But I brought it up-to-date; I took into account what had taken place a year before at the Bretton Woods Conference.

Of the sixteen books I have written, “Inflation is Coming!” is the only one which became a best-seller. A little less than half a million copies were sold. I used to be amused when I visited a book store I patronized down in Wall Street to see two stacks of books side by side, one of my “Inflation is Coming!” and another by a Wall Street analyst, W. J. Baxter, entitled “No Inflation Is Coming!” Both seemed to be selling equally well.

In spite of immense sale of my book, in the thirty years since it was published nobody in power in Washington and nobody in the prevailing Keynesian establishment has paid any attention to my call for the establishment of a stable dollar. Irving Fisher, of Yale, to whom they should have listened, had been calling for a stable dollar for years. He had enlisted the support of some of the most influential economists, bankers and business leaders both here and in England. They formed an association to promote the idea. But he had no more influence on official policy than someone as little known as myself.

But those who are making monetary policy today ought to be listening. If they believed Fisher “dated” and that his ideas are irrelevant today, they ought to listen to what Chancellor Jacques Rueff, of the French Academy, who is one of France’s most distinguished economists, spelled out in detail in the book he published in 1972 entitled “The Monetary Sin of the West”. In his book he says, and includes the evidence to prove it, that the inflation which was started in 1944 is now irreversible and that it is going to end in one of the worst catastrophes in the whole economic history of the world.

They ought not only to be listening but also doing something about it. But they are doing neither.

***

The idea of conducting a series of experiments to demonstrate the feasibility of creating an inflation-proof monetary system, instead of writing another book about inflation, came to me on March 3rd, 1972. At that time my wife and I were wintering at a resort near Escondido, California, and I was working on a book I planned to call “Wealth and Ilth”.

On March 3rd—I made note of the day on what came to be called the Escondido Memorandum— was in Escondido looking up some material for my book at the library. While eating lunch I picked up and began to read a copy of the New York Times. Like the rest of the press that day, the Times featured under banner headlines the crisis caused by the first devaluation of the dollar. For days representatives of the International Monetary Fund from all over the world had been meeting at the Smithsonian Institute in Washington, trying to decide what to do about it.

It suddenly occurred to me that an experiment to do what neither my own book nor the books of my friend Irving Fisher had done, might rivet attention on the importance of replacing the present unstable and inconstant dollar with a stable and constant one. I made some notes about what such an experiment would entail, finished them when I got back to the ranch and my typewriter, and decided that if I could persuade the two banks in Exeter, New Hampshire, where I lived, to make it possible for me to launch such an experiment, I would do so.

Both banks, perhaps, because they both knew me, agreed to make it possible for me to conduct an experiment. The experimenting then began. I began to create a complex alternate currency system which was to include the issuance of bank-money, the printing of paper money, and the minting of a coinage. The whole system was to be based upon a substitute for the dollar to be called a “constant.”

The first constants were issued at a conference of about three hundred people in Conway, New Hampshire, on June 21st, 1972 called together to discuss “The Human Future” by the School of Living of Freeland, Maryland. The last constant was issued in the summer of 1973, when I was convinced that the feasibility and acceptability of the idea of such an alternative currency had been proved, and I felt, because of my age, unable to transform what was an experiment into an international bank of issue.

I want to take this opportunity to thank the hundreds of people all over the United States—beginning with those who bought the first constants at Conway—whose cooperation made the Exeter experiments possible. Perhaps this account of my experiments may eventually lead to transforming what they helped to do into a viable stable alternative currency system; perhaps it may lead some one or some group with the administrative talent, necessary resources, the statistical and banking “know-how”, to create an international bank to issue the constant.

What their cooperation proved is that there must be hundreds of thousands of worried victims of inflation, and perhaps millions who are ready to abandon the dollar the moment an alternative like the constant becomes available.

Chapter 4: The Exeter Experiments

The Exeter experiment began on my return from California in April 1973. Once the experimenting began, the number of different kinds of experiments needed to establish the feasibility and the acceptability of the idea kept increasing.

What became plain as they proceeded is that all three of the forms in which money is issued—bank-money, paper money, and coinage—called for experiments of many kinds if the proper method of issuing them was to be established. It was this fact which made it necessary to change almost everything we did from time to time until experience finally made clear the best way of doing it.

What also became plain when I began to plan the experiments was that two problems had to be solved before even the first experiment could be conducted: (1) the problem of eliminating political control and government interference, and (2) the problem of how to support a bank which issued a currency based upon a commodity reserve without turning for support to ulterior interests either corporate or governmental in nature.

The idea of a commodity-backed currency has always labored under two disadvantages. The “Proposals for an International Commodity Reserve Currency” submitted to the conference at Bretton Woods by the Committee for Economic Stability of which the two Grahams were leading members—Frank D. Graham who wrote “Fundamentals of International Policy” and Benjamin Graham who wrote “World Commodities and World Currency”—labored under both disadvantages.

The first was that all of the advocates of such a currency, including the Grahams, took it for granted that the currency would be issued and controlled by the same kind of central banks which now issue the money used everywhere in the world.

The second was that the cost of storing a commodity reserve was plainly prohibitive. The cost of providing a reserve of gold or silver, because they took up little room, was so low that their use seemed practicable. The cost of storing a reserve which included commodities such as wheat and rice was so that their use as a reserve seemed utterly impractical.

Both disadvantages disappeared in the approach to the problem upon which the Exeter experiments were based. The first disappeared when the plan adopted for the experiments rejected the idea that governmental central banks should have anything to do with the issuance of the new currency. The second disappeared when the cost of storing the reserve was eliminated by arbitraging it whenever possible instead of storing and immobilizing it. Instead of burdening the bank-of-issue with costs of storage, the costs of storage would be borne, as is the case today, by the users of the commodities—by the mills and industries which process basic commodities and by the importers and exporters who ship them from producer nations to consumer nations. When a mill buys wheat to process it into flour, it pays for the cost of storage during the time it was stored by the growers and includes this cost in the price it charges to the consumers of flour. When an importer in Britain buys wheat from an exporter in Australia, the cost not only of storage in Australia but also of “storage” while it is in transit, is included in the price the importer pays for the wheat.

The elimination of government central banks eliminates political considerations and national interests from the issuance of money. The elimination of costs of storage by resorting to arbitrage not only makes the use of commodities as a reserve practicable but provides an income which will help to make the bank-of-issue self-supporting. Unless such a bank is entirely independent and completely self-supporting, it would have to turn to the government for support or to other ulterior vested interests. Instead of being free to render a necessary service, impartially it would find itself being used either to promote private special interests or to promote what the politicians in control of the government call the national interest.

This plan eliminates both of these objections. It eliminates political considerations and national interests from the issuance of money. It makes it possible to avoid taxes and other hindrances in nearly every country, including the United States, on the movement of funds from one country to another. By substituting an independent bank-of-issue chartered in some country like Luxembourg (which does not interfere with currency movements) for a government controlled central bank, the needs of trade rather than the needs of the government would be served. There are several countries like Luxembourg and the proposed bank-of-issue might actually incorporate in several of them so that it could move from one to another if one of them tried to interfere with its operations.

Initially I believed that all the essential experiments could be finished within a year. This might have been possible if my resource had been large enough. Working only as fast as my limited resources permitted, it took another six months to reach the point when it was no longer necessary to think of the creation of an alternative stable monetary unit such as the constant as experimental in nature.

To include a detailed account of all the experiments is not a part of the plan of this book. But to give the readers of it some “feel” for what took place, I believe the best thing is to include one of the best of many stories which appeared in various magazines and newspapers both here and in England. What follows was a feature story written by Mel Most, the Financial Editor of The Bergen Sunday Record, of Hackensack, New Jersey. It occupied a full page in its issue of February 4, 1973. Mel Most took a particular interest in the matter because I used to live in his neighborhood and he knew something about me. This is his story, word for word:

Would you believe—a new, worldwide, inflation-proof money? Pensions, insurance benefits, and annuities paid in the dollar value of the day they were signed for? Imports and exports that arrive with prices unaffected by shifts in exchange rates after they were ordered? Wages that adjust by themselves to the rising cost of living?

Ask Dr. Ralph Borsodi, an author-economist who shook up Rockland County with his social experiments when he was a mere 50 and is doing the same to Exeter, N.H. at 86.

He’s been quietly testing a currency designed to keep pace with prices — suddenly spotlighted by recent headlines:

President Nixon’s lifting most wage-price controls; a 20-year record, one month jump in wholesale prices; the cost of food expected to go up 50 per cent higher than forecast for the first half of this year.

For seven months, Borsodi has had Exeter shoppers, merchants, banks, and schools paying and receiving with monetary units he calls ‘Constants’ used like dollars.

Thousands of dollars of bank money orders and personal checks for Constants have circulated like money, been used for buying and selling, and have been cashed by tellers.

The big difference is that regular money buys less and less as time passes, while the Constant is pegged in value to the government’s cost-of-living index. That means one Constant should always buy the same amount of goods on the average.

For example, people who bought Constants from Borsodi’s organization at say, $2.18 a 10-Constant note, were surprised later when the bank gave them $2.19 for it. That was because the cost of living index had risen by a half-percent or so in the meantime.

The experiment worked so well in the sleepy New England town of 8,892 inhabitants that the University of New Hampshire Press in Durhanif is printing a first issue of 275,000 Constants in currency form.

Now worth about 22 cents a Constant, the bills will go into circulation next month—with coins to follow—in denominations of CI, C5, CIO, C25, and C100. The Constant is designated by ‘C’ crossed with an ‘equal’ sign.

‘We need something more stable than all the paper currencies today which are really nothing but overdrafts’ Borsodi said. ‘The Constant will be pegged to the price of commodities.”

Backing it, he said, are enough capital reserves—$100,000—to cover an unheard of, sudden 10-point rise in the cost of living index. The interest alone has undoubtedly been enough to pay for the test runs, although it won’t provide the permanent basis of operation. Backing the project, too, has been a lot of confidence—the indispensable ingredient that make currencies rise and fall in value.

Even the staid, wealthy Philips Exeter Academy prep school paid in Constants for thousands of dollars of printing and supplies.

Joining his following among businessman, volunteers come halfway across the country from Borsodi’s other disciples—the youth.

Youths rebelling against the urban-suburban rat race have rediscovered his book on homesteading in Rockland County, Flight from the City, republished almost 30 years after it spurred a back-to-the-land movement in the Suffern area during the Depression. Borsodi left Rockland County in the early 1950’s.

Another book written by Borsodi during his 33 years of homespun living in Rockland warned that ‘Inflation is Coming” and led to the Constant.

‘Inflation is the meanest of all tragedies’, he said. ‘It strikes the old who have counted on their savings.’

Borsodi, an energetic, wiry man, walks every morning to his office at Independent Arbitrage International, his non-profit organization which issues and redeems the Constant. He almost always goes home for lunch with Mrs. Borsodi, whose picture is prominent on his desk.

As conservative in dress as he is radical in his monetary theory, Borsodi was flanked by two college-age office volunteers and admirers, Richard Sexton from Memphis, Tenn., and F. Paul Salstrom from Rockport, Ill.

Up to now, the Constant has been backed by the $100,000 reserve, which is on deposit at banks in Exeter, Boston and London. The plan is funded by users themselves, since they pay or deposit money with the organization to get their Constants.

First National Bank of Boston and two Exeter banks confirmed that Independent Arbitrage International (I AI) was a substantial depositor and was considered responsible. Besides Borsodi as chairman, its advisory committee includes bankers, brokers, editors, attorneys and economists.

In a new phase, the organization has incorporated in Luxembourg—where there are no restrictions on movement of money—to form an international banking institution which will be completely free of any government’s needs.

‘The difficulty with the International Monetary Fund is that they use it to finance the government’s deficits. We’ll be doing a banking job instead,’ Borsodi said.

In place of capital based on payments and reserves, he plans to base the Constant on goods—and instead of being pegged to the government price index, it will be pegged to the world price of those goods.

Here’s how the idea works. Suppose a fanner puts aside a $1,000 profit on his summer harvest to pay for cattle feed next winter. By the time the winter comes, the feed may cost $1,100 and he is short $100.

Instead, if he got title to the feed right away, he’d have it in the winter at no extra cost, no matter what the price then is. In fact, he would sell his title for $100 more than he paid for it.

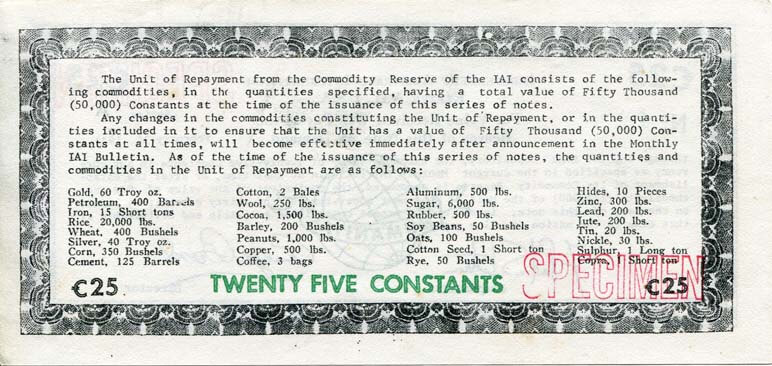

Arbitrage proposes to make each Constant a title for a tiny share, not just in a single commodity such as feed, but in the 30 top commodities in world trade.

What these commodities sell for ultimately affects most world prices, and as their price average went up, so would the value of the Constant based on it.

IAI doesn’t intend to store any goods, or to speculate in commodities futures on the markets. Commodities arbitrage (rhymes with ‘garage’) is a form of simultaneous trading in different places. It serves buyers and sellers as an international clearinghouse and saves on shipping goods back and forth, if they can be supplied locally.

‘We’re interested only in spot (immediate) commodities—no storage expense, no speculation,’ Borsodi said. ‘You make money, you have an income from it.

Now the Constant will be backed by actual commodity values in arbitrage, adjusted monthly to a price index based on world trading prices in the 30 commodities since the mid-1960’s.

Prof. William R. Hosek, IAI economist at the Whitemore School of Business Administration of the University of New Hampshire, has just completed computer work on a sort of ‘Dow Jones’ index of the 30 commodities price averages.

Gold and silver prices, which used to be the sole basis of most of the world’s currencies, come back merely as two of the nine most traded metals, including aluminum, copper, iron, lead nickel, tin and zinc.

The index also includes the world’s 13 main food staples—barley, cocoa, coffee, copra (dried coconut meat), com, cottonseed, oats, peanuts, rice, rye, soybeans, sugar and wheat. Its other commodities are cement, cotton, hides, jute, petroleum, rubber, sulphur, and wool.

Hosek is enthusiastic about prospects.

‘The idea of the scrip is to have a currency that doesn’t depreciate as prices go up/’ he said. ‘It’s a test to see whether or not it would be acceptable and whether the people would hold and use the stuff. It clears through the bank like a check written in dollars.’

Asked if a savings account wouldn’t appreciate as much just on bank interest, Hosek shook his head: ‘You can’t use a savings account for carrying out transactions. You use a checking account. A checking account in dollars today, with just enough in it to buy a TV set, won’t buy a TV set three months from now.

But some bankers arc less than enthusiastic about the new issue of scrip, although they participated in the earlier system of using Constants as a money-of-account

Edwin R. Baker, Vice-President of Exeter Banking Company, which participated in the initial tests, said: ‘I do think there’s some basic merit in Dr. Borsodi’s original concept. If you’re dealing in dollars with a foreign business that may take three months to deliver, a businessman signs a contract for $2,000 and finds he has to pay $2,200. Or, if not, it’s the seller who has to lose money on it.’

He added: ‘Dr. Borsodi doesn’t expect a recession this year, but he believes it’s bound to come. If it docs, maybe we’ll all find he’s right about money. Part of the merit of the dollar is that it’s based on faith—when the faith is a little bit shaken, the fate of the dollar is affected.’

One merchant put it more baldly: ‘Maybe people will call it a funny money scheme, but the question is whose money is funny—his or ours?’

Baker’s bank won’t be involved in the scrip issue, but he told how Borsodi’s two-state tests worked.

The first was a check device, with amounts printed in Constants—10, 50, or 100. They circulated in town in thousands of dollars worth. Nobody questioned them. When they were cashed against the IAI account, the check was endorsed and we filled in the dollar amount, around $2.18 for $10, to start with.

‘Sometimes people filled in their own and made mistakes. With 50’s, the mathematics can get a little hairy.’

Borsodi then tested individual checking accounts in Constants, which are continuing.

‘Each person maintains an account in his own name with IAI,’ Baker explained. ‘Dr. Borsodi takes care of the individual accounts. As far as the bank is concerned, we treat them all as one account with many signatories. There are close to 50, mostly local, but we’ve also got some scattered around—New Jersey, Maryland, even one in Alaska.’

‘It worked perfectly all right because the system for clearing checks has been part of our financial system for many years.’

The problems with the scrip will be that there is no individual endorser, Baker said. He also wondered about how the capital gains would be taxed as it went up in dollar value—presumably like a bearer bond, to be taxed when the gain is realized.

The biggest legal headache for a small bank, he said, was whether the scrip could circulate as currency. ‘Technically, they’re promissory notes.’

However, no objection was seen by Deputy Chief Counsel Westbrook Murphy at the Office of the United States Controller of the Currency, when reached in Washington:

‘They can circulate clamshells or pine cones if they want to, as long as people accept them. There’s plenty of Canadian money circulating in Northern New Hampshire.’

‘The law only provides that you have a right to demand payment in US currency as legal tender if you want to.’

Murphy did dig up an old law, intended to protect the coinage, which makes it a misdemeanor to issue anything intended to circulate in place of money, for less than SI.

That would affect only the 1-Constant denomination if carried out. But it would also prevent, for example a New York newsstand dealer from accepting or making change in subway tokens, and other common practices.

Borsodi is taking no chances.

‘We’re assuming that once this thing gets started,’ he said, ‘this is going to frighten the Treasury and the Federal Reserve System. It’s going to reflect upon the fact that we Americans are issuing a currency that’s being inflated.’

What had made him think of the idea? ‘In one study, I found some people had lost between five and ten percent of the purchasing power of savings they put into government savings bonds, which could only buy less at maturity than when they were acquired.’

When I decided that I had to discontinue the experiment I had started, I prepared a series of position papers which those who wanted to carry on with the idea might find useful. I can think of no better report on the results of the experiments than these position papers. All of them are here included, revised only enough to make them fit into a book which any intelligent layman, and not only a monetary economist, can understand.

The first dealt with the nature of inflation.

Chapter 5: On the Nature of Inflation

Nothing is more ironic than the fact that among the perhaps millions of words written about inflation, there is not one definition of the word, so far as I know, of which it might be said that it makes (a) what inflation is, (b) how it comes into existence, and (c) why it is so injurious to mankind so clear that its victims are moved to do something about it.

The explanation for this has its source in a curious fact: the fact that no meaningful definition of inflation is possible without defining its antithesis, deflation. And no meaningful definition of either inflation or deflation is possible without the definition of a word which designates a money supply which is neither inflated nor deflated.

Irving Fisher suggested the use of the word “stabilization” for this purpose. For a number of reasons I decided the best word to use was “normalization”. Normalization suggests what should take the place of both inflation and deflation, and normal can properly be used to designate a money supply which is neither too large nor too small, which is therefore neither inflated nor deflated.

1. Inflation: Inflation occurs when the money supply is increased by issuing money for such purposes as: for meeting the deficits of a government; for capital investments, for speculation of any kind, for loans to buy or hold stocks, bonds, realty and other securities; for the development and modernization of underdeveloped nations; or for stimulating business or reducing unemployment. Under these circumstances the increase is inflationary, the money supply is inflated, and prices of all kinds raised.

The failure of the government to interdict by law such inflation of the money supply is governmental nonfeasance and misfeasance; the act of the government itself in creating such inflation, malfeasance.

Inflation, since it stimulates speculation, is uneconomic, and since it cheats all those who work and all those who save, dishonest.

2. Deflation: Deflation occurs when the money supply is decreased by a refusal to issue money when needed to those properly entitled to borrow it, or when the interest rate is raised to deliberately discourage production. Under these circumstances the decrease is deflationary, the money supply is deflated, and the price level pushed downward.

When the freedom of banks to issue money, particularly during a depression, is restrained or forbidden by any activity of the government (this is government misfeasance and nonfeasance) or the government permits such restraint by permitting the private monopolization and centralization o banking (this is government nonfeasance and malfeasance) deflation is not only made possible but inevitable.

Deflation, since it reduces production, is uneconomic and since it cheats all those who either borrow money or produce goods, it is dishonest.

3. Normalization: Normalization occurs when the total money supply is maintained by issuing or retiring money in circulation so that it provides for all the short term needs, but only for the short term needs, of the producers and distributors of goods. Under these circumstances the money supply is normal. With normalization, the price level tends to be stabilized; the price level tends neither to rise or fall because of anything done or undone by the issuers of money; speculative exploitation of the banking system is made virtually impossible, and wages and profits tend to rise only as productivity is increased.

Since such a money supply is both honest and economic, neither inflation nor deflation, no matter how excused and rationalized is excusable.

If for the moment we postpone answering in detail what money should and should not be issued for until that question comes up later, then normalization of an inflated money supply calls for the retirement of money which should not have been issued at all; normalization of a deflated money supply calls for the issuance of new money which should have been issued to avoid deflation, while normalization of a normal money supply calls for the maintenance of a money supply which is already providing all the money properly needed—neither more nor less.

Chapter 6: On the Nature of Money

There is nothing more astonishing than the fact that those who ought to know most about the nature of money— including the central bankers who issue it and the monetary authorities and economists who supposedly know all about it—have the foggiest notions about what money in actuality is.

There are two reasons for this: (1) the fact that the truth about its nature is obscured by the complexity of the ways in which it comes into existence, and (2) the fact that, because of this, it is defined in all the texts on economics and in all the dictionaries and encyclopedias not in terms of what it is but in terms of what it is used for. To dispel this obscurity a whole book would be needed; to define it properly only a few paragraphs.

Existing definitions state that money is a medium of exchange, that it is a measure of value, that it is a store of value, and so on ad infinitum. None of these statements are true. They state not what money is factually but what money is used for functionally. A pencil can be used to scratch one’s head, but this does not justify anybody in saying that a pencil is a head-scratcher. No matter how used, a pencil is a pencil.

What money in reality is, is a claim. It is a claim in the same sense that bills and invoices, promissory notes and mortgages, and entries of accounts receivable in a ledger are claims against those who are obligated to pay the bills, the notes and the accounts they owe to those to whom they owe them.

But it is a claim which differs from all other kinds of claims in four ways: (1) the holder’s claim is a claim against the government or bank-of-issue whose money he has accepted; (2) the money itself may consist either of bank-money on deposit in a bank, printed notes, or coinage; (3) the holder of the money is entitled to the redemption of his claim in full on demand; and (4) the value of the goods or services he can buy with the redemption must be the same as the value of the goods he sold or the services he rendered when he accepted the money. If the value is either more or less, cheating takes place. If its purchasing power has been reduced, those who use it to buy are cheated; if it has been increased, those who accept it in selling are cheated.

True, when money is used to buy and sell things it is used as a medium of exchange. True, when it is used to put a price on something, it is used as a measure of value. And true, when it is stored in a tin box or safe for future use, it is used as a store of value. But no matter how used, it is none of these things. No matter how often it changes hands and no matter how different the uses made of it, it remains at all times a claim against the original issuer of the money.

***

Money, is not, however, just a claim the repudiation of which injures only the claimant. Repudiation, even if only partial, injures everybody who has or uses money. Inflation of the money supply is such a partial repudiation. Only the issuer benefits from this; everybody else loses by it. It injures everybody who uses the money because it raises the price level by making everybody pay more money for the same goods and because it reduces the purchasing power of everybody who earns money or saves it.

For the full significance of the fact that money is a claim to be appreciated, it is important to bear in mind that this is what not only the United States but all the nations which are members of the IMF are ignoring. What they are doing is in effect a form of massive repudiation of honest claims which should be fully and honestly redeemed. What they are doing should not be called inflation; it should be called legalized embezzlement.

***

While all the many kinds of money used throughout the world are claims—each nation has its own kind—the fact that there are three basic kinds of money must be taken into account and positions with regard to each of them taken. These three basic kinds of money consist of what will be called in the terminology of this study (1) bank-money, (2) paper-money, and (3) metal-money.

Chapter 7: On the Issuance of Money

All the different kinds of money in use today (the dollar, the pound, the franc, the mark) and all the different kinds used since money was first invented (coins, paper-money, bank-money), have obviously had to come into existence and have had to be issued in some way. Inflation will never be properly dealt with and the evils for which it is responsible never corrected until the way in which money is now issued and the way in which it should be issued is understood.

To understand what is right and wrong in the issuance of money, it is of the utmost importance never to forget that it came into existence for only one reason, to make it possible to replace bartering with buying and selling. The fact that this is habitually ignored by both the masses of people who use money and by the central bankers and the treasury department officials who issue it is responsible for most of the monetary confusion and most of the monetary evils which call to high heaven for correction.

In bartering only two parties are involved. Each barterer has something the other party wants, and the transaction is consummated when each exchanges what he does not want for what he does. But in buying and selling three parties are involved: the buyer, who pays for what he wants with money, the seller, who accepts the money, and the issuer of the money used. In such a transaction, the seller exchanges the goods which he sells not for other goods but for a claim (evidenced by the money) which he can later use to buy what he then wants.

What will be called commerce in this book will refer to transactions of this kind. For the sake of ending the existing confusion about money, the word commerce ought to be used for no other purpose.

That in modem nations this third party, the issuer of the money, behaves like an unscrupulous scoundrel is proved by the fact that he not only inflates the money but sometimes deflates it; by the fact that this cheats the holder of the money when the holder finally spends it.

The process of cheating begins when the money is issued. This is what makes understanding the issuance of money so important.

Issuance, as the term will be used in this discussion, refers to the activities of central banks, in the United States the Federal Reserve System, in the minting, printing, creating and circulating of money. The machinery used in doing this is so complicated that it would take a book of its own to describe it. AH that is essential for the purposes of this study is to make clear why the issuance of money for improper purpose—for such a purpose of growth and development, for instance—makes inflation not only possible but possible as a deliberate policy. Keynesianism, as I have tried to make clear, is the rationalization of inflation as a deliberate policy.

The crucial question is what is back of the money which the central banks operating on Keynesian principles issue? There is some gold of course, but today gold reserves are not only trifling but for the most impounded. Most of it is “backed” by loans which should never be made—loans made to monetize the debts of the government; loans made to finance war and the military-industrial complex; monetize the securities of giant corporations which should not exist at all, and to finance speculations in securities, commodities and land. Finally there is back of it money issued to finance the needs of commercial banks in making legitimate commercial loans. Insofar as the debts discounted and monetized in this way really consist of loans made for legitimate commercial purposes, there is no abuse involved. But most of the loans discounted by commercial banks, just like those made directly by central banks, are made to finance precisely the same activities which should not be monetized at all.

What I have called the monetization of debts here is just another way of saying the issuance and circulation of money. The means by which the money issued is circulated is provided by payments made for labor employed, for the commodities used, and for the capital equipment purchased by ail these borrowers.

Now what must never be overlooked to understand what is going on are two things: that all the money issued and circulated in this complicated fashion consists of claims held by those who have accepted the money and that it is the banks-of-issue which are ultimately responsible for the redemption of these claims.

The position which I am taking with regard to issuance is based upon five positive and six negative principles all of them in turn based upon the above two indisputable facts: (a) the fact that money consists of claims, and (b) the fact that the banks which issue the money are responsible for redeeming the claims.

The five positive principles are:

The issuance of money is a banking and not a government function. The establishment of the monetary-unit, the determination of its unit of redemption, the printing of the currency, and the minting of the coinage are functions which should be performed by a bank-of-issue organized for service and only to serve the needs of commercial banks in making legitimate commercial loans.

The only proper purpose for the issuance of money is to facilitate the buying and selling of commodities and merchandise.

The money issued should have a constant and unvarying purchasing power.

The money supply must be increased or decreased only in accordance with the volume of trade. There are no circumstances which justify or which make it really necessary to issue money for any other purpose.

The money supply should not become legal tender for the payment of debts by the ipse dixit of the government but by agreement between the buyers and sellers who use the money issued by the third party to all monetary transactions.

The negative principles are:

It must never be issued to provide money for capital investments by anybody or to provide capital for any kind of enterprise no matter how apparently desirable. It must never be issued to finance capital investments in land and buildings, machinery and durable production equipment, stocks and bonds, or loans and mortgages on such investments.

It must never be issued to finance the growth of developed economies (such as that of the United States) or development of the economies of underdeveloped nations (such as that of India).

It must never be issued to finance government debts.

It must never be issued to finance charitable, educational, religious, or other non-commercial enterprises.

It must never be issued to provide employment, reduce unemployment, or support the unemployed.

It must never be issued to finance personal loans or finance consumer purchases.

Chapter 8: On the Redemption of Money

The term redemption as it will be used in this study refers to the only honest conclusion to the series of transactions initiated when a bank—any bank-of-issue anywhere—issues money which is accepted and which circulates until some one who holds it decides for any reason whatsoever to redeem or retire it. Retirement means not only redemption but also extinction. If the redemption is to be honest, the bank must in the end deliver to the holder of the money the same amount of purchasing power as the amount for which it was originally issued. When the purchasing power is reduced by inflating the money supply on Keynesian principles, as it is being reduced in the modem world, the holder of the money is cheated. Redemption, unless it is to continue being dishonest, must be the act of restoring to the holders of money the value of what they gave—neither more nor less—when they accepted the money.

Though almost never explicitly stated on the money now issued and used today, redemption by the bank which originally issues it is always implied. No failure to state it on the money issued relieves the bank from the obligation created by its issuance. The fact that the users of the money temporarily relieve the bank of its obligation by continuing to use and circulate it does not relieve the bank of the ultimate obligation of redemption and retirement.